FIRST PRINCIPLES:

FIRST PRINCIPLES:

Let’s start with what a loan actually is.

A loan is a product.

Like any product, someone has to make it, deliver it, and not go broke doing it.

The “price” of a

loan is the interest rate.

That price has to cover three things:

- the cost to acquire the borrower

- the cost to service the loan

- and the losses from people who can’t pay it back.

Now here’s the math that matters.

A $300 loan at 36% APR for two weeks generates $4.15 in interest.

That’s it.

Four dollars and fifteen cents to cover the cost of underwriting a stranger with no credit score, processing the transaction,

handling collections when it goes sideways, and absorbing the losses from the 15-20% of borrowers who default.

You

cannot build that business at $4.15 per transaction.

Not with staff.

Not with software.

Not with regulatory compliance.

Not with anything.

So the lender doesn’t try.

They leave.

THE PERFECT ANALOGY:

THE PERFECT ANALOGY:

Imagine your city passes a law capping taxi fares at $2 per ride, no matter the distance.

Sounds great for riders, right?

Except every cab company in the city does the same math in five minutes and parks its fleet.

No driver will work for $2 a ride.

The economics don’t exist.

Now the people who needed cheap rides, the ones without cars, the ones who can’t afford Uber surge pricing, the ones working night shifts, they’re not protected by the $2 cap.

They’re stranded.

The cap didn’t make transportation affordable.

It made transportation disappear.

That’s

the 36% APR cap.

It doesn’t make small-dollar credit cheaper. It makes small-dollar credit vanish.

HOW IT ACTUALLY WORKS:

HOW IT ACTUALLY WORKS:

Here’s the sequence, step by step.

Step 1: The law passes.

Politicians celebrate.

Consumer advocates declare

victory.

Press releases go out about “protecting vulnerable borrowers.”

Step 2: Lenders do the math.

They already know what Illinois found out, what Colorado found out, what every

state that ran this experiment found out.

You cannot profitably originate a $300-$500 short-term loan at 36% APR.

The revenue doesn’t cover the cost structure.

Step 3: Lenders exit.

Not because they’re evil.

Because they’re not charities.

Licensed, regulated lenders, the ones following the rules, filing the disclosures, operating with state oversight, close their doors or stop offering the product.

Step 4: The borrower still has the emergency.

The car still needs fixing.

The utility is still getting shut off.

The

prescription still costs $87.

Tuesday still comes.

Step 5: The borrower finds alternatives.

And here’s where “consumer protection” creates the real damage.

The alternatives are:

- overdraft fees (effectively 3,000%+ APR on a $35 NSF charge)

- pawning property

- borrowing from family (with relationship costs that don’t show up in data)

- loan sharks with no disclosures and no regulators, or simply not solving the problem, which means losing the job, paying the reconnect fee, skipping the medication.

-

Step 6: The data looks clean.

Payday loan volume drops.

Regulators declare VICTORY.

Nobody tracks what happened to the borrower after the lender left.

WHY IT MATTERS:

WHY IT MATTERS:

The subprime borrower experiencing a sudden financial emergency is not choosing between a payday loan and a savings account.

They’re choosing between a payday loan and a worse option.

Remove the payday loan, and they don’t get the savings account.

They get the worst option.

Illinois implemented the 36% cap.

Lenders left.

Storefronts closed.

The consumers who needed $300 to keep their lights on found themselves with fewer licensed locations than they had before the “protection” arrived.

The real loan

sharks:

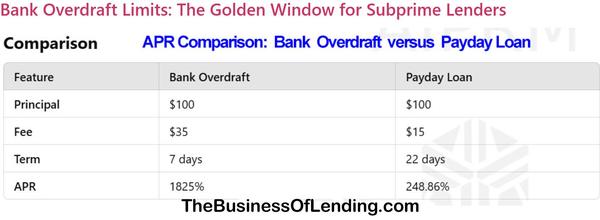

A $35 NSF fee on a $100 overdraft, returned in three days, is a 4,258% APR.

Nobody protests that number.

It doesn’t fit the narrative.

FAQs & COMMON CONFUSIONS:

FAQs & COMMON CONFUSIONS:

Confusion 1: “High APR means predatory.”

APR was designed to compare 30-year mortgages.

Applied to a 14-day loan, it’s a mathematical distortion.

The actual dollar cost of a $300 payday loan is typically $45-$60.

The APR looks monstrous because you’re annualizing a two-week fee.

Compare dollar cost to dollar

cost, not annualized rates on products built for different time horizons.

Confusion 2: “Banks will fill the gap.”

Banks abandoned this market decades ago.

Small-dollar, short-term lending to credit-challenged borrowers is not profitable at bank cost structures.

If banks wanted this customer, they’d have them already.

Confusion 3: “Online lenders will step in.”

Some will.

Unregulated ones.

Operating offshore.

Without state oversight,

without disclosure requirements, without collection limits.

The cap doesn’t eliminate demand.

It pushes demand underground.

Confusion 4: “People shouldn’t need these loans.”

That’s a statement about a world that doesn’t exist.

In the world that does exist, 40% of Americans cannot cover a $400 emergency from savings.

Policy has to start with reality, not with the life we wish people were living.

TEST YOUR UNDERSTANDING:

TEST YOUR UNDERSTANDING:

Question 1: If a 36% APR cap is implemented nationally, what happens to a borrower who needs $300 on a Friday to fix her car by Monday so she doesn’t lose her job?

If your

answer includes “she’ll find a cheaper loan somewhere,” you missed it.

The cheaper loan doesn’t exist for that credit profile.

She finds a worse option, or she doesn’t solve the problem.

Question 2: Who benefits from the 36% APR cap?

Borrowers with good enough credit to qualify for bank products. Credit unions. Politicians who need a clean headline. Nobody at 580 FICO with a broken alternator.

Question 3: What’s the difference between restricting credit access and protecting consumers?

Protection means the consumer ends up safer.

Restriction means the product disappears.

They are not the same thing.

One requires tracking what happens after the regulation.

The other just requires passing the

law.

The bottom line, stripped to the bone:

You cannot legislate cost out of a transaction.

You can only legislate who bears it.

The 36% APR cap moves the cost from “a disclosed fee on a licensed product” to “a crisis the borrower solves however they can.”

That’s not protection.

That’s just paperwork that lets someone else feel good about a problem they didn’t solve.

THE ONE-SENTENCE ESSENCE: A 36% APR cap doesn’t protect subprime borrowers from expensive credit; it removes their access to credit entirely, then calls that

protection.

THE ONE-SENTENCE ESSENCE: A 36% APR cap doesn’t protect subprime borrowers from expensive credit; it removes their access to credit entirely, then calls that

protection.